Stocks Gain as Earnings Roll In; Treasuries Climb: Markets Wrap

Here are the main moves in market:

Stocks

- Futures on the S&P 500 Index gained 0.3% as of 8:34 a.m. New York time.

- The Stoxx Europe 600 Index rose 0.4%.

- France’s CAC 40 Index climbed 0.5%.

- The U.K.’s FTSE 100 Index dipped 0.3%.

- Turkey’s Borsa Istanbul 100 Index surged 1.6%.

Currencies

- The Bloomberg Dollar Spot Index was little changed.

- The British pound climbed 0.2% to $1.2636.

- The euro sank 0.2% to $1.1004.

- The Turkish lira climbed 0.9% to 5.8753 per dollar.

- The Japanese yen was little changed at 108.35 per dollar.

Bonds

- The yield on 10-year Treasuries dipped three basis points to 1.69%.

- The yield on two-year Treasuries declined four basis points to 1.55%.

- Germany’s 10-year yield dipped one basis point to -0.47%.

- The Canada 10-year government bond yield dipped four basis points to 1.47%.

Commodities

- West Texas Intermediate crude declined 0.4% to $53.38 a barrel.

- Gold was little changed at $1,493.04 an ounce.

- Arabica coffee fell 0.6% to $0.94 a pound.

- LME nickel surged 2.2% to $16,920 per metric ton.

U.S. stocks were poised to open higher after strong earnings reports from several of America’s largest banks. Treasuries jumped as trading resumed after a holiday.

Futures on the three main equity indexes all rose alongside stocks in Europe, defying concern Beijing and Washington remain far apart in their quest for a trade deal. In earnings news:

- JPMorgan’s third-quarter results beat estimates.

- Goldman Sachs reported investment bank revenue and earnings per share that undershot estimates, but its equities sales and trading was a beat.

- BlackRock said there was a decline in fixed income inflows from the previous quarter as clients moved some money back into equities.

- Wells Fargo’s EPS missed estimates; Citigroup’s adjusted EPS and FICC trading revenue were both a beat.

- Johnson & Johnson raised its sales and earnings forecast for the year.

Futures earlier trimmed some of their advance as Bloomberg reported China may not buy the volume of American goods proposed in the “phase one” trade deal. Earlier Japan’s gauge had jumped as trading resumed after a long weekend during which President Donald Trump announced progress on an interim accord with China. Markets elsewhere in Asia were mixed. The Stoxx Europe 600 Index rose, with 18 of 19 sectors advancing led by retailer shares.

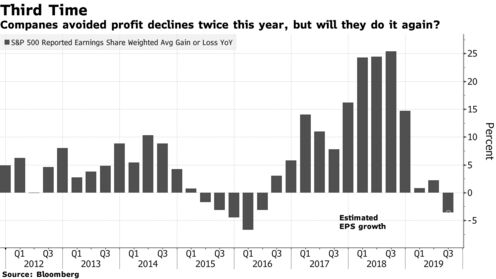

As the U.S. earnings season begins in earnest, investors are closely analyzing the reports, given the global backdrop of slowing growth and a host of unpredictable macro risks from the impeachment investigation into Trump and the trade war to Brexit and Turkey’s incursion into Syria.

The pound strengthened as British negotiators submitted a revised set of Brexit plans to Brussels amid growing optimism that a deal could be struck this week. The euro slipped as data showed investor confidence in Germany’s economic outlook remains weak. Crude oil futures fluctuated and gold drifted.

Meanwhile, the Turkish lira jumped and the country’s benchmark stock index rose after Trump imposed milder penalties over its military campaign in Syria than U.S. lawmakers had demanded.

Here are some key events coming up this week:

- Wednesday brings a monetary policy decision in South Korea.

- U.S. retail sales are forecast to increase for a seventh straight month. Sales in the “control group” are also expected to rise. Consumer spending is carrying the weight of U.S. economic growth so the data will be monitored closely for any signs of slowing.

- China releases third-quarter GDP, September industrial production and retail sales data on Friday.